By Patrick Kuster, AIF

When it comes to deciding which accounts should own which investments, there is a common misconception that your portfolio’s largest-expected-return investments should always be purchased within your Roth IRA. In other words, there is a highly accepted rule-of-thumb to avoid lower-yielding investments within your Roth and to always target maximizing income tax-free growth. But this decision shouldn’t be one-dimensional, and your asset location strategy should strive to optimally balance your after-tax expected return with your after-tax expected risk.

The Traditional Approach

Roth IRAs experience income tax-free distributions, and as there are no required minimum distributions (RMDs), your investments can continue to grow until you decide to take out funds (or your beneficiaries are forced to one day distribute the funds). Further compounded by some of the indirect benefits of Roth IRAs – such as distributions not counting toward adjusted-gross income, which could potentially keep you eligible for certain deductions or avoid increased Medicare costs – we can understand why many are quick to conclude that prioritizing growth within the Roth IRA is most efficient.

But this approach isn’t always optimal. The waters get muddy when a non-retirement account (such as a joint account) is introduced to the mix, as Uncle Sam generally participates in the risk of non-retirement account investments but doesn’t with Roth IRA investments. As I previously discussed, owning $1 of a stock in your Roth IRA, where you bear all the risk, isn’t the same as owning $1 of the same stock in a joint account. And when we adjust for this difference in risk, we may conclude that it’s optimal to prioritize some riskier investments to a non-retirement account instead of to the Roth IRA.

Focusing on Taxes

The level playing field of expected investment returns is how much you expect, at the end of the day, to be in your pocket and not Uncle Sam’s (i.e., the after-tax expected return). Calculating the after-tax expected return is a critical step in determining an optimal asset location strategy, and depending on your financial situation and individual investments, it could be rather complex.

Taxable (Non-Qualified) Accounts

Taxable accounts, such as joint accounts, receive preferential tax rates on long-term capital gains and qualified dividends, as well as other potential tax advantages on investment vehicles like limited partnerships, while interest income receives the higher ordinary income tax rate. This is the fundamental reason bonds and tax-inefficient investments are generally prioritized to tax-deferred and retirement accounts (such as traditional IRAs and Roth IRAs).

For taxable accounts, you don’t receive 100% of the expected return (unless you’re in a 0% tax bracket), and therefore Uncle Sam bears some of the risk.

Traditional IRAs

For traditional IRAs, taxes are deferred so Uncle Sam only collects when funds are distributed from the account. From your point of view, your traditional IRA receives and compounds 100% of the pre-tax expected return on “your” portion of the traditional IRA (the portion that won’t be paid to Uncle Sam). Yes, Uncle Sam’s portion goes up and down, and yes, it’s in your account, but the only reason you care at all about his portion is because you’re both invested the same way. You’re both cheering for the same team.

This is also to say that you receive 100% of the pre-tax expected return on your portion of the portfolio, and you take on 100% of the risk of your portion of the traditional IRA. Uncle Sam receives 100% of his portion as well and takes risk on 100% of his portion. Therefore, we don’t adjust pre-tax expected returns or risk for taxes when compounding, as we only “grow” your portion of the portfolio (the traditional IRA balance less the imbedded tax-liability due to Uncle Sam in the future).

Roth IRAs

For Roth IRAs, this math is simple; there are no income taxes to consider, so the after-tax expected return is the expected return. You receive 100% of the pre-tax expected return, and you bear 100% of the risk on the entire Roth IRA balance.

Putting it All Together

Deciding which account should own which investment is more of a process than a blanket statement or rule of thumb.

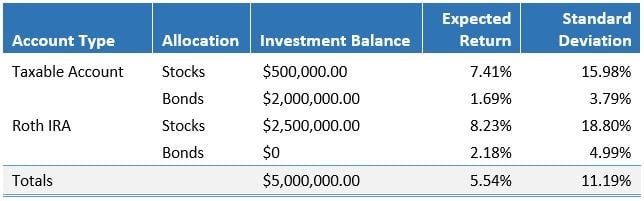

Let’s take the example of John and Jane Doe, who have a $5 million portfolio consisting of diversified stocks and bonds. Following the traditional approach, they’ve prioritized their tax inefficient bonds to the IRAs and have placed their highest-expected-return investments (their diversified stocks) in their Roth. They are in the 24% income tax bracket, 15% long-term capital gains (LTCG) bracket, and we’d like to look at their portfolio’s expected after-tax balance in five years.

For the illustrative purposes of our article, we will assume stocks are taxed at LTCG rates annually (this assumes 100% turnover essentially every 366 days; a rather aggressive assumption for stocks), and that all interest and bond income is taxed at ordinary income rates.

After years of Roth conversions, John and Jane Doe have a $2.5 million Roth IRA and a $2.5 million joint (taxable) account. With stocks prioritized to the Roth IRA, their portfolio is allocated like this:

This portfolio has an expected, after-tax value of $6,603,188.80 in five years.

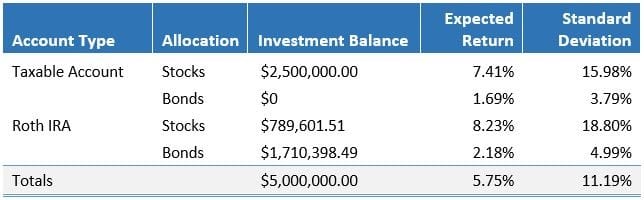

If we filled the taxable account with stocks first and then solved for the amount of stocks in the Roth IRA that would keep the after-tax standard deviation to 11.19% (that is, to the same after-tax expected risk):

Our expected, after-tax value increased by about $49,100 in five years to $6,652,290.78 while maintaining the same amount of after-tax risk. It’s worth noting in this example that the portfolio increased its stock allocation by about $290,000, but, as Uncle Sam participates in an additional $2 million of stock risk (now in the taxable account), the overall risk exposure of John and Jane Doe remains the same.

Special Considerations

There are some instances where the asset location decision requires extra caution and consideration. As an example, if you anticipate using all or a portion of your traditional IRA funds for future Qualified Charitable Distributions (QCDs), it may be best to “carve out” the current traditional IRA assets you’ll put toward this future QCD, as the charity is taking on the risk of these funds and essentially the after-tax rate for you is 0%.

Impact

Traditional approaches to asset location are impactful when deciding between traditional and Roth IRAs. Placing tax inefficient investments in IRAs, either traditional or Roth, is generally favorable for most investors. However, when deciding between taxable accounts and IRAs, higher-expected-return (and therefore generally higher-risk) investments demand greater attention. Just because a Roth IRA has income tax-free properties does not mean you are always better off taking 100% of the investment risk.

By risk-adjusting your portfolio, you can use the asset location decision to potentially increase expected after-tax return or to decrease expected after-tax risk. Either way, properly implementing a strategy to optimize asset location enhances the efficiency of your portfolio and increases the probability of your financial plan’s success.

About the author: Patrick Kuster, AIF®

As a Wealth Advisor with Buckingham Strategic Wealth, Patrick Kuster, AIF®, knows that even the most thorough and well-conceived financial life plan is only as good as its implementation. He works closely with clients to help them solve their financial puzzle – pulling apart plans, rebuilding them, then seeing them through – and achieve their most important retirement goals.

Important Disclosure: The opinions expressed by featured authors are their own and may not accurately reflect those of Buckingham Strategic Wealth®. This article is for general information only and is not intended to serve as specific financial, accounting or tax advice. The examples provided are for illustrative purposes only and do not reflect any specific client’s experience. Return information is for example purposes only. Investing involves risk including loss of principal. Individuals should speak with qualified professionals based upon their unique circumstances. The analysis contained in this article may be based upon third-party information and may become outdated or otherwise superseded without notice. Third-party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. IRN-21-1974

Got Questions About Your Taxes, Personal Finances and Investments? Get Answers!

Email Jeffrey Levine, CPA/PFS, Chief Planning Officer at Buckingham Wealth Partners, at: