After a year that most of us want to forget, 2021 is shaping up to start with stability and an even keel. The election is safely behind us, the new Biden Administration promises a ‘no drama’ approach, a closely divided and hyper-partisan Congress is unlikely to enact any sweeping legislation, reform or otherwise, and COVID vaccines are ready for distribution. It’s a recipe for a calm news cycle.

Which makes it a perfect time to buy into the stock market. Investors can read the tea leaves, or study the data – whatever their preferred mode of stock analysis – and use this period of calm to make rational choices on the stock moves.

Using the TipRanks database, we’ve pulled up three stocks that present a bullish case. All three meet a profile that should interest value investors. They hold unanimous Strong Buy consensus ratings, along with a ‘perfect 10’ from the Smart Score. That score, a unique measure, evaluates a stock based on 8 factors with a proven high correlation to future overperformance. A ‘10’ score indicates a strong likelihood that the stock will rise in the coming year. And finally, all three of these stocks present with double-digit upside potentials, indicating that they are still undervalued.

UMH Properties (UMH)

We’ll start in the real estate investment trust (REIT) sector, with UMH Properties. This company, which started out after WWII in the mobile home industry, later become the premier builder of manufactured housing. Today, UMH owns and manages a portfolio of 124 manufactured housing communities, spread across 8 states in the Northeast and Midwest, and totaling well over 23,000 units.

As a REIT, UMH has benefitted from the nature of manufactured houses as affordable options in the housing market. UMH both sells the manufactured homes to residents, while leasing the plots on which the properties stand, and leases homes to residents. The company’s same-property income, a key metric, showed 8.6% year-over-year increase in the third quarter.

Also in the third quarter, UMH reported a 16% yoy increase in top line revenue, showing $43.1 million compared to $37.3 million in the year-ago quarter. Funds from Operations, another key metric in the REIT sector, came in at 11 cents per share, down from 14 cents in 3Q19. The decrease came as the company redeemed $2.9 million in Series B Preferred Stock.

REIT’s are required to return income to shareholders, and UMH accomplishes this with a reliable dividend and a high yield of 4.7%. The payment, at 18 cents per common share, is paid quarterly and has been held stable for over a decade.

Compass Point analyst Merrill Ross believes the company is in a sound position to create value for both households and shareholders.

“We believe that UMH has proven that it can bring attractive, affordable housing to either renters or homeowners more efficiently than has been possible with vertical rental housing. As UMH improves its cost of funds, it can compete more effectively with other MH community owners in the public and private realms, and because it has a successful formula to turn around undermanaged communities, we think that UMH can consolidate privately-owned properties over the next few years to build on its potential for value creation,” Ross opined.

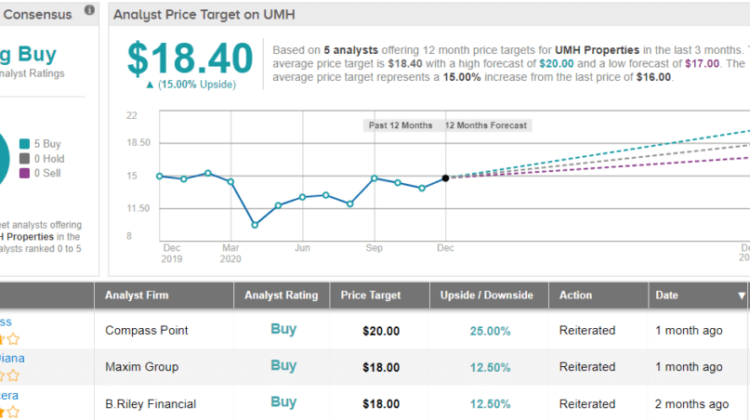

To this end, Ross rates UMH a Buy, and her $20 price target implies a 25% one-year upside. (To watch Ross’s track record, click here)

Overall, the unanimous Strong Buy on UMH is based on 5 recent reviews. The stock is selling for $15.92, and the $18.40 average price target suggests it has room for 15% growth from that level. (See UMH stock analysis on TipRanks)

Laird Superfood (LSF)

Laird Superfood is a newcomer to the stock markets, having gone public just this past September. The company manufactures and markets a range of plant-based, nutrient-dense food additives and snacks, and is most known for its line of specialized non-dairy coffee creamers. Laird targets customers looking to add nutrition and an energy boost to their diet.

Since its September IPO, the company has reported Q3 earnings. Revenue was strong, at $7.6 million, beating the forecast by over 26% and coming in 118% above the year-ago figure. The company also reported a 115% yoy growth in online sales. Ecommerce now makes up 49% of the company’s net sales – no surprise during the ‘corona year.’

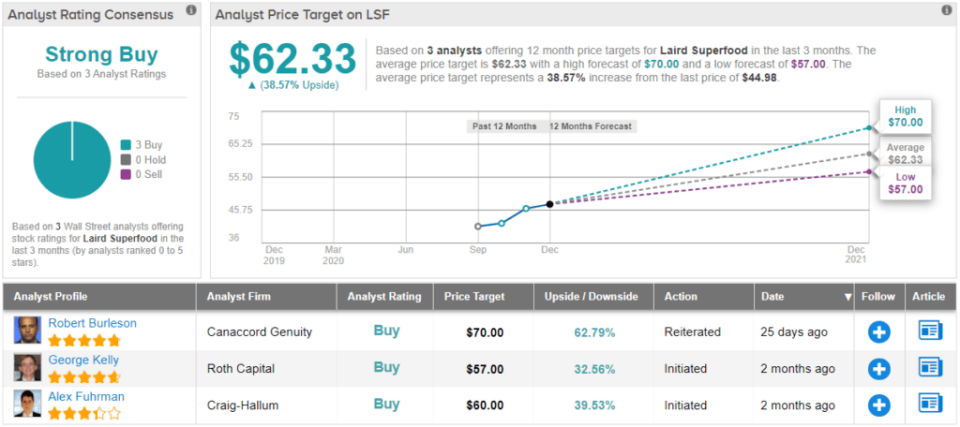

The review on the stock comes from Robert Burleson, a 5-star analyst from Canaccord. Burleson reiterates his bullish position, saying, “We continue to view LSF as an attractive platform play on strong demand trends for plant-based, functional foods, noting LSF’s competitively differentiated omni-channel approach and ingredients ethos. Over time, we expect LSF to be able to leverage its brand and vertically integrated operation into success in a broad range of plant-based categories, driving outsized top-line growth and healthy margin expansion.”

Burleson rates LSF shares a Buy alongside a $70 price target. This figure indicates his confidence in ~63% growth on the one-year horizon. (To watch Burleson’s track record, click here)

Laird has not attracted a lot of analyst attention, but those who have reviewed the stock agree with Burleson’s assessment. LSF has a unanimous Strong Buy analyst consensus rating, based on 3 recent reviews. The stock’s $62.33 average price target suggests room for ~39% upside in the coming year. (See LSF stock analysis on TipRanks)

TravelCenters of America (TA)

Last but not least is TravelCenters of America, a major name in the transportation sector. TravelCenters owns, operates, and franchises full-service highway rest stops across the US – an important niche in a country that relies heavily on long-haul trucking, and in which private car ownership has long encouraged the ‘road trip’ mystique. TA’s network of rest stops offers travelers convenience stores and fast-food restaurants in addition to gasoline and diesel fuel and the expected amenities.

The corona crisis has been hard time for TA, as lockdown regulations put a damper on travel. The company’s revenues bottomed out in Q2, falling to $986 million, but rose 28% sequentially to hit $1.27 billion in Q3. EPS, at 61 cents, was also strong, and showed impressive 165% year-over-year growth. These gains came as the economy started reopening – and with air travel still restricted, automobiles become the default for long distance, a circumstance that benefits TravelCenters.

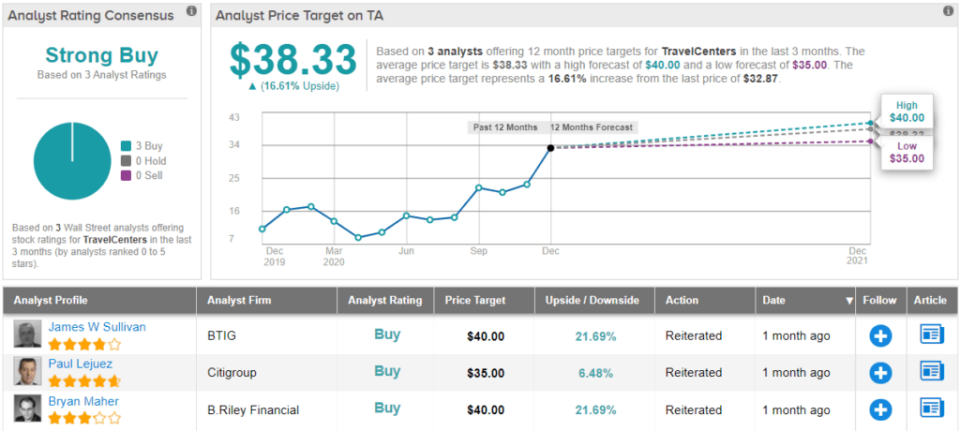

Covering TravelCenters for BTIG is analyst James Sullivan, who rates the stock a Buy, and his $40 price target suggests a 22% upside over the coming year. (To watch Sullivan’s track record, click here)

Backing his stance, Sullivan noted, “TA is in the process of moving on from a series of unsuccessful initiatives under the prior management team. The current new management team has strengthened the balance sheet and intends to improve operations through both expense cuts and revenue-generating measures which should boost margins […] While we expect the 2020 spend to be focused on non-revenue generating maintenance and repair items, we expect in 2021 and beyond that higher spending should generate good ROI…”

All in all, TravelCenters shares get a unanimous thumbs up, with 3 Buys backing the stock’s Strong Buy consensus rating. Shares sell for $32.87, and the average price target of $38.33 suggests an upside potential of ~17%. (See TA stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.