At long last, the annus horribilus 2020 is coming to an end, and it’s time to get our portfolios in order for the new year ahead. There is good news about to encourage investors for 2021. In proof that government sometimes can move with speed and decision, FDA granted emergency authorization for both the Pfizer and Moderna COVID vaccines, and the shots are getting into the distribution networks. The election is settled, except for the Georgia Senate runoffs, but no matter how those turn out the overall results is known: a closely divided government, without a clear mandate for sweeping legislation. It’s a portent of regulatory stasis, which means predictability, which is good for markets.

These are the facts behind the rising investors sentiment, which has pushed the Dow Jones, the S&P 500, and the NASDAQ all up to record levels. And its’ that upbeat sentiment which has Wall Street’s top analysts selecting stocks as potential winners for the year ahead.

And when we say it’s Wall Street’s top analysts making these calls, we mean it. These are stock picks from the 3 top-ranked analysts in the TipRanks database. These are the stock experts with the most recommendations on file, the best success rate, and the highest average return. So, let’s see what they have to say about these three Strong Buy stocks.

ZoomInfo Technologies (ZI)

Tech companies, especially in the cloud, communications, and marketing segments, have some clear opportunities during the COVID pandemic. ZoomInfo is part of this group; the company’s services include digital marketing intelligence, account and data management, demand generation, and lead prospecting. ZoomInfo offers AI cloud software designed to makes these background tasks more efficient, so that sellers can focus on selling.

ZI shares have seen volatile trading since going public in June of 2020, but overall, the stock is up 34% year-to-date.

The third quarter, ZoomInfo’s first full quarter as a public company, showed strong results to encourage investors. Top line revenue hit $123.4 million, up 11.8% sequentially and 56% year-over-year. EPS, which had been negative in Q2, turned positive in Q3 with a 2-cent per share profit. The company finished the quarter with $59.8 million in free cash flow. ZoomInfo reported having 720 customers with $100,000 or more in annual contract value.

In his review of ZoomInfo, Piper Sandler’s Brent Bracelin, rated the #1 analyst on Wall Street by TipRanks, lays out a straightforward bullish case.

“We are raising revenue estimates by $13.6M for this year and $19.6M for next year factoring in broad-based strength and minor contributions from Everstring and Clickagy acquisitions. We are buyers of ZI based on its ambitions to build a modern go-to-market (GTM) operating system with a unique business model balancing high-growth and high margins… Based on strong Q3 results and favorable Q4 outlook, we would be aggressive buyers of ZI given its unique profile of a high-growth and high-margin model with limited downside risk,” Bracelin opined.

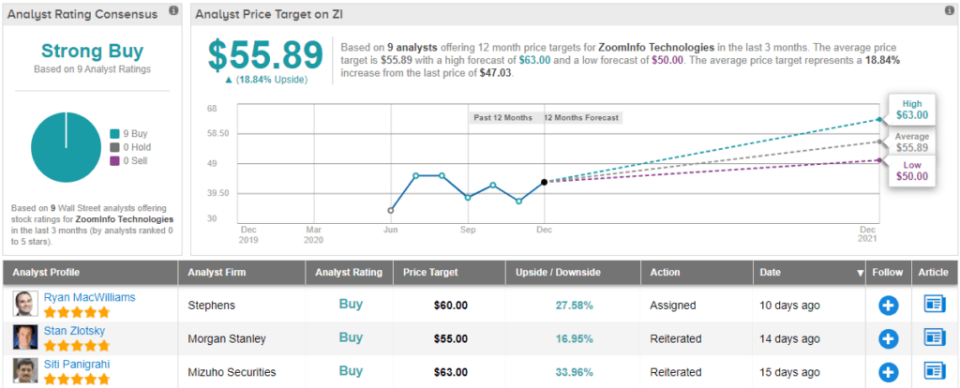

Bracelin sets a $59 price target to go along with this Overweight (i.e. Buy) rating, suggesting that ZI has room for ~25% growth next year. (To watch Bracelin’s track record, click here)

Overall, there are 9 recent reviews on record for ZoomInfo and all are Buys – making the analyst consensus rating a unanimous Strong Buy. Shares are priced at $47.03 and the average price target of $55.89 indicates ~19% upside potential from that level. (See ZI stock analysis on TipRanks)

Ichor Holdings (ICHR)

Next up is a holding company, whose subsidiaries design, engineer, and manufacture gas and chemical fluid delivery systems essential in a variety of industries. Ichor is best known for its contributions to the semiconductor industry’s capital equipment, where its gas module and chemical process subsystems make up a substantial portion of each chip’s cost. Ichor’s systems are also used in the manufacture of LED displays, biomedical equipment, and alternative energy sources.

Specialized manufacturing can be a solidly profitable niche, especially when a company is building parts and tools necessary to top-line industries. Semiconductor chips are essential in the digital world, and they cannot be manufactured without input from Ichor’s tools. This gives Ichor a competitive advantage, as it offers a product that its customers cannot do without.

This can be seen in the quarterly revenues, which have been rising slowly but steadily through 2020. The company saw $220 million at the top in Q1, and reported $228 million in Q3. The third quarter was up 47% year-over-year, and was the sixth quarter in a row to show sequential gains. EPS, at 45 cents per share, was up 28% yoy.

Among the fans is Needham’s Quinn Bolton, who’s ranked #2 on Wall Street, according to TipRanks.

“[We] believe Ichor’s fundamentals remain strong… we expect the offering will enable ICHR to pursue meaningful accretive M&A that should strengthen its market position, accelerate revenue growth and provide for vertical integration and higher gross margin over time. Looking further out, should the company achieve its LT operating model over the next ~3 years, we see NG earnings power of $4.85 per share,” Bolton commented.

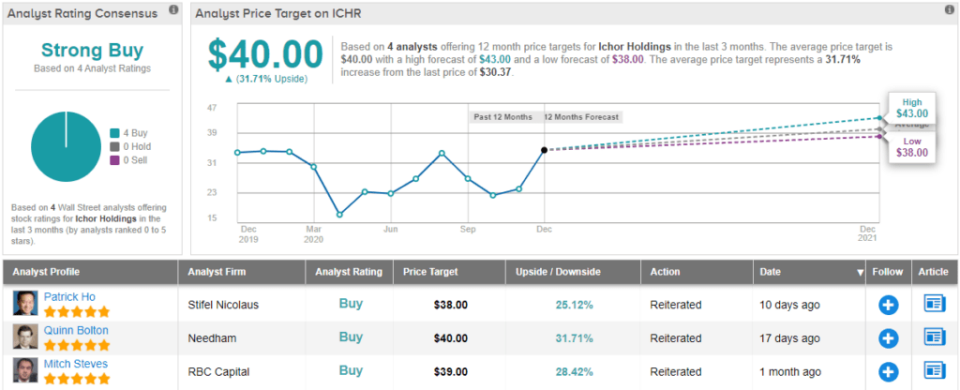

To this end, Bolton rates the stock a Buy, and his $40 price target implies a one-year upside of 32%. (To watch Bolton’s track record, click here)

Like Bolton, Wall Street is picking ICHR as a long-term winner. With 4 unanimous Buy ratings assigned over the last three months, the stock earns a Strong Buy analyst consensus. Adding to the good news, its $40 average price target puts the upside potential at ~32%. (See ICHR stock analysis on TipRanks)

DocuSign (DOCU)

Last but not least is DocuSign, the cloud-based electronic signature service from San Francisco. DocuSign offers customers a verified and secure electronic signature option for online documents. Customers reap savings from efficiency, in the form of faster turnaround, less ink and paper used in printing, and less time spent printing and distributing hard copies for signature.

DocuSign shares have seen a steep appreciation in 2020, as the move toward remote work and virtual offices put a premium on digital services and online verification. DOCU is up 205%, more than tripling its value this year.

The stock has gained as the company’s revenues have gone up. The top line rose 29% between Q1 and Q3, with the third quarter number hitting $382.9 million. Earnings in the third quarter were up an impressive 53% year-over-year. The yoy increase in free cash flow was even more impressive, turning from negative $14 million to a surplus of $38 million.

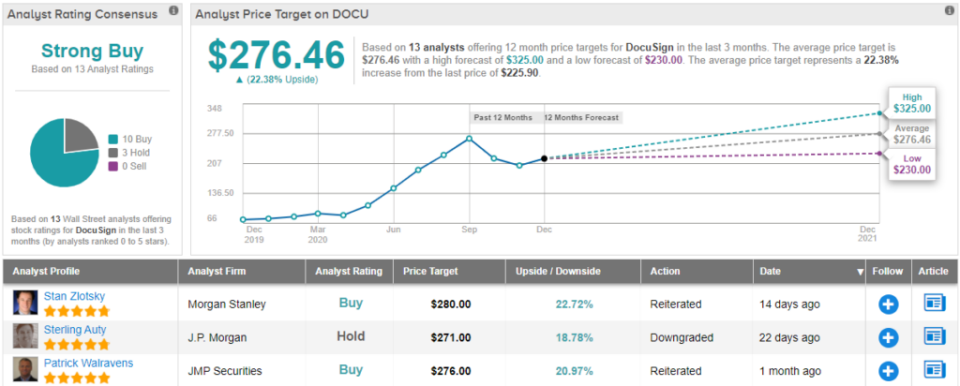

All of this leads RBC’s Alex Zukin, the #3 analyst in the TipRanks database, to rate DOCU an Outperform (i.e. Buy) along with a $325 price target. Investors stand to pocket a 44% gain should the analyst’s thesis play out. (To watch Zukin’s track record click here)

Backing his stance, Zukin writes, “[The] Beats go on as DOCU delivered another very strong quarter of acceleration on every metric… What is even more impressive in our minds is that this is being driven almost entirely by an acceleration of the core e-signature business with the company being confident that it is still very modestly penetrated in its TAM (which has expanded significantly) that they can maintain growth above pre-pandemic levels in a post-pandemic world…”

Similarly, other Wall Street analysts like what they’re seeing. With 10 Buy ratings vs 3 Holds received in the last three months, the stock earns a Strong Buy consensus rating. At a $276.46 average price target, analysts see ~22% upside potential in store for DocuSign. (See DOCU stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.